AGNICO EAGLE MINES mit 50% Potenzial

| eröffnet am: | 20.02.08 11:26 von: | Wolle1307 |

| neuester Beitrag: | 12.04.26 18:29 von: | MrTrillion3 |

| Anzahl Beiträge: | 183 | |

| Leser gesamt: | 140116 | |

| davon Heute: | 87 | |

bewertet mit 3 Sternen |

||

|

|

||

01.11.21 08:10

#101

chivalric

bin dankbar

hier nochmals zum Zug gekommen zu sein :)

buy the dip ^^

keine Empfehlung zu irgendwas

buy the dip ^^

keine Empfehlung zu irgendwas

13.01.22 08:22

#103

DaveK

Ja, Minenschliessungen sind doof ...

... aber ich Stimme da dem Aktionär schon zu: Besser jetzt kontrollierte Restriktionen versuchen als dann monatelange Schliessungen zu mit höherer Wahrscheinlichkeit in Kauf zu nehmen.

Grds. ist Corona überall schlecht und führt zu reduzierten Produktionen oder beeinträchtigt diese irgendwie.

Derzeit ist aber Agnico immer noch für mich das Beste, was es im Sektor gibt, weil die Minenen nicht in Dritte-Welt-Diktaturen liegen. Und insgesamt hält sich der Kurs auch unter Berücksichtigung der Übernahme ja gut. Schlussendlich ist fast nur der Goldpreis von Relevanz ...

Grds. ist Corona überall schlecht und führt zu reduzierten Produktionen oder beeinträchtigt diese irgendwie.

Derzeit ist aber Agnico immer noch für mich das Beste, was es im Sektor gibt, weil die Minenen nicht in Dritte-Welt-Diktaturen liegen. Und insgesamt hält sich der Kurs auch unter Berücksichtigung der Übernahme ja gut. Schlussendlich ist fast nur der Goldpreis von Relevanz ...

20.01.22 21:57

#104

neymar

Agnico Eagle Mines

Jaime Carrasco discusses Agnico Eagle Mines

https://www.bnnbloomberg.ca/video/...usses-agnico-eagle-mines~2364905

https://www.bnnbloomberg.ca/video/...usses-agnico-eagle-mines~2364905

24.01.22 08:36

#105

DaveK

Sehr kurzes Interview ...

... der Herr Carrasco findet aber den Wert und die Übernahme gut. Danke für den Link.

25.01.22 13:38

#106

KnightRainer

......

Agnico=Bester Senior Producer.

Ende Februar kommen erstmals konsolidierte Zahlen mit Kirkland. Das wird eine Zeitenwende.

Tiedje uund andere EW´ler sehen Gold bis 15000USD steigen. Unklar ist nur, ob Gold vorher nochmal unter 1700 absackt oder nicht. Am Ziel ändert das nichts.

Ende Februar kommen erstmals konsolidierte Zahlen mit Kirkland. Das wird eine Zeitenwende.

Tiedje uund andere EW´ler sehen Gold bis 15000USD steigen. Unklar ist nur, ob Gold vorher nochmal unter 1700 absackt oder nicht. Am Ziel ändert das nichts.

24.02.22 21:37

#107

MrTrillion3

CA0084741085 - Agnico Eagle Mines

Agnico Eagle Mines Limited (AEM) CEO Ammar Al-Joundi on Q4 2021 Results - Earnings Call Transcript

SeekingAlpha, heute - inkl. Tonaufnahme

24.02.22 21:40

#108

MrTrillion3

CA0084741085 - Agnico Eagle Mines

News Release auf der Webseite von AEM

24.02.22 21:42

#109

MrTrillion3

CA0084741085 - Agnico Eagle Mines

"Quarterly dividend increased by 14% – A quarterly dividend of $0.40 per share

has been declared (previous quarterly dividend was $0.35)" (s. News Release weiter oben)

has been declared (previous quarterly dividend was $0.35)" (s. News Release weiter oben)

25.02.22 10:07

#110

neymar

Agnico

Inflation always creates environment where gold does well: Agnico Eagle's Sean Boyd

https://www.bnnbloomberg.ca/video/...agnico-eagle-s-sean-boyd~2389992

https://www.bnnbloomberg.ca/video/...agnico-eagle-s-sean-boyd~2389992

17.03.22 09:46

#111

DaveK

Dividende per heute gutgeschrieben ...

... auf's Jahr gerechnet sind es mit Kurs von heute, ca. 55 Euro, runde zwei Prozent Dividendenrendite. Für einen Minenbetreiber nicht schlecht, finde ich. Schöne Grüße an die Leute im Forum.

19.09.22 13:28

#114

neymar

Agnico Eagle

Copper-zinc project with Teck does not change our gold strategy: Agnico Eagle CEO

https://www.bnnbloomberg.ca/video/...trategy-agnico-eagle-ceo~2522787

https://www.bnnbloomberg.ca/video/...trategy-agnico-eagle-ceo~2522787

29.09.22 23:06

#115

nicco_trader

Trenwende?

Leider mit Gap

Kaufempfehlung von Taylor Dart, 28.9.

https://seekingalpha.com/article/...-smart-move-to-boost-the-pipeline

Kaufempfehlung von Taylor Dart, 28.9.

https://seekingalpha.com/article/...-smart-move-to-boost-the-pipeline

Angehängte Grafik:

agnico_20220929.png (verkleinert auf 40%)

agnico_20220929.png (verkleinert auf 40%)

28.10.22 11:54

#116

neymar

Agnico Eagle

Agnico Eagle CEO sees another strong quarter on production and cost control

https://www.bnnbloomberg.ca/video/...duction-and-cost-control~2551115

https://www.bnnbloomberg.ca/video/...duction-and-cost-control~2551115

07.11.22 20:47

#117

MrTrillion3

CA0084741085 - Agnico Eagle Mines

Habe heute nochmal ein paar Stücke nachgelegt. Zielbestand damit jetzt endgültig erreicht. Ab hier heißt es, den Goldrausch abzuwarten - wann immer er kommen möge.

Eins steht fest: An Kryptos glaube ich nicht und

Eins steht fest: An Kryptos glaube ich nicht und

28.11.22 22:10

#118

MrTrillion3

CA0084741085 - Agnico Eagle Mines

AGNICO EAGLE PUBLISHES FIRST CLIMATE ACTION REPORT

")

NEWS PROVIDED BY

Nov 28, 2022, 08:00 ET

25.02.23 11:10

#119

nicco_trader

A Softer 2023 Outlook

Taylor Dart, 17. Feb.

Auszug

"

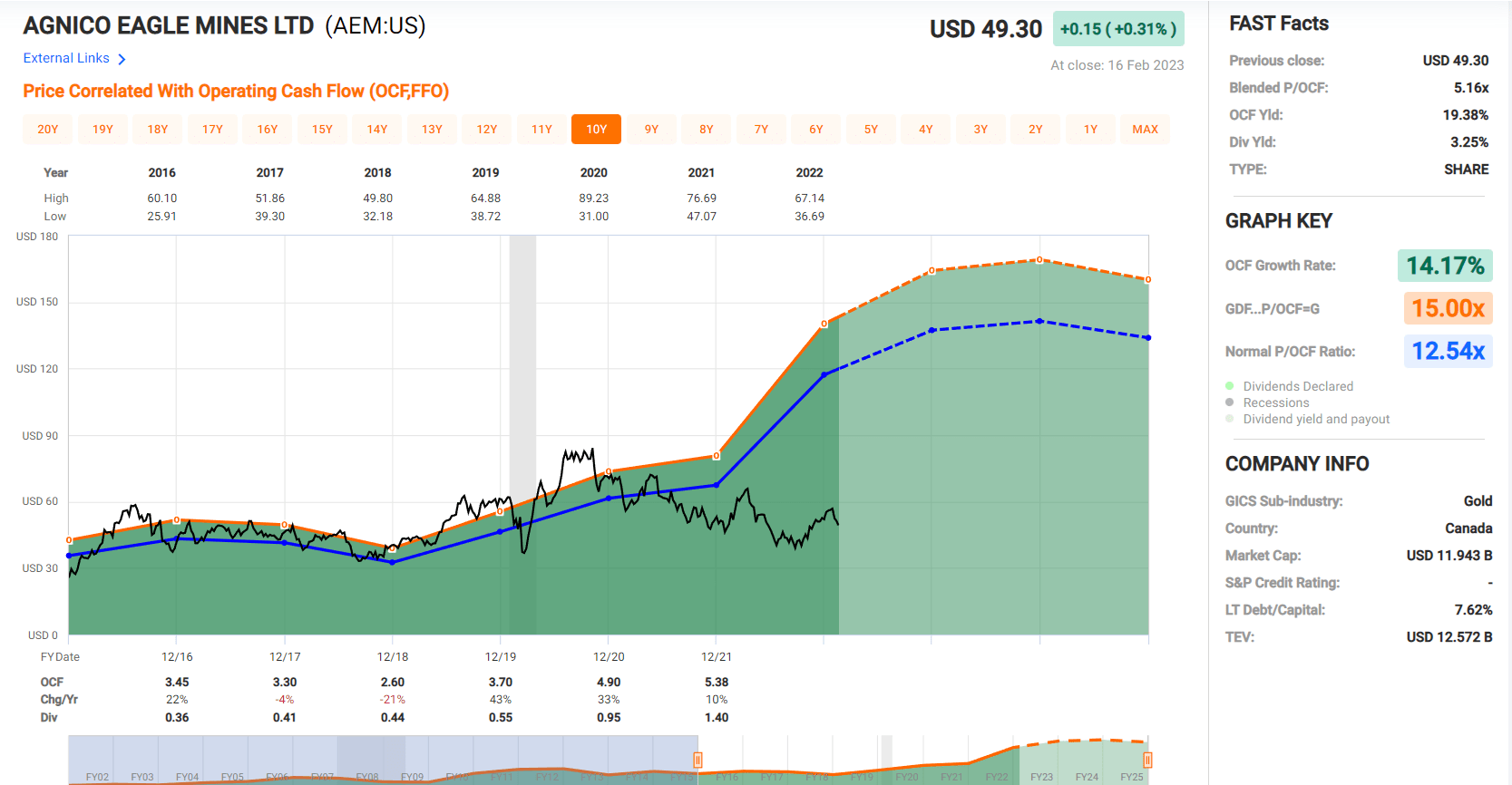

Looking at the chart above , Agnico has historically traded at 12.5x cash flow, and I would argue that a multiple of 13.0 is more than reasonable, given that it's the premier major producer with favorable jurisdictions and attractive margins. Based on conservative FY2023 cash flow estimates of $4.50, this translates to a fair value for the stock of US$58.50, pointing to 20% upside from current levels. However, this fair value estimate is based on what will be a weak year for Agnico, and it doesn't place any value on its strong development pipeline or exploration upside, where I think we can easily assign a value of $5.0+ billion (Santa Gertrudis, Upper Beaver, Wasamac, Hammond Reef, Hope Bay, San Nicolas [50%], exploration upside). It also doesn't place any value on organic growth at existing assets like Detour Lake."

"Given that valuing the stock on cash flow understates the company's long-term potential, I believe the best way to value Agnico Eagle Mines Limited stock is on a P/NAV basis. Based on an estimated net asset value of ~$23.7 billion after adjusting for G&A expenses, and assigning a 1.45x P/NAV multiple given its strong history of reserve replacement, I see a fair value for Agnico stock of ~$35.0 billion. After dividing by ~490 million shares (year-end 2023), this translates to a fair value for the stock of US$71.40, translating to a 44% upside from current levels or ~47% upside on a total return basis.

Importantly, this doesn't account for upside in the gold price, with these assumptions based on a $1,700/oz gold price, in line with the three-year average. Given its undervaluation, I continue to see Agnico as one of the best buy-the-dip candidates sector-wide."

Chart Cashflow

https://static.seekingalpha.com/uploads/2023/2/17/...38073_origin.png

https://seekingalpha.com/article/...eagle-mines-a-softer-2023-outlook

******

Prognosen

https://www.marketscreener.com/quote/stock/...ITE-1408914/financials/

******

Saisonalität: Bodenbildung im März, Hoch August

https://charts.equityclock.com/...le-mines-ltd-nyseaem-seasonal-chart

Auszug

"

Looking at the chart above , Agnico has historically traded at 12.5x cash flow, and I would argue that a multiple of 13.0 is more than reasonable, given that it's the premier major producer with favorable jurisdictions and attractive margins. Based on conservative FY2023 cash flow estimates of $4.50, this translates to a fair value for the stock of US$58.50, pointing to 20% upside from current levels. However, this fair value estimate is based on what will be a weak year for Agnico, and it doesn't place any value on its strong development pipeline or exploration upside, where I think we can easily assign a value of $5.0+ billion (Santa Gertrudis, Upper Beaver, Wasamac, Hammond Reef, Hope Bay, San Nicolas [50%], exploration upside). It also doesn't place any value on organic growth at existing assets like Detour Lake."

"Given that valuing the stock on cash flow understates the company's long-term potential, I believe the best way to value Agnico Eagle Mines Limited stock is on a P/NAV basis. Based on an estimated net asset value of ~$23.7 billion after adjusting for G&A expenses, and assigning a 1.45x P/NAV multiple given its strong history of reserve replacement, I see a fair value for Agnico stock of ~$35.0 billion. After dividing by ~490 million shares (year-end 2023), this translates to a fair value for the stock of US$71.40, translating to a 44% upside from current levels or ~47% upside on a total return basis.

Importantly, this doesn't account for upside in the gold price, with these assumptions based on a $1,700/oz gold price, in line with the three-year average. Given its undervaluation, I continue to see Agnico as one of the best buy-the-dip candidates sector-wide."

Chart Cashflow

https://static.seekingalpha.com/uploads/2023/2/17/...38073_origin.png

{kind=link}

https://seekingalpha.com/article/...eagle-mines-a-softer-2023-outlook

******

Prognosen

https://www.marketscreener.com/quote/stock/...ITE-1408914/financials/

******

Saisonalität: Bodenbildung im März, Hoch August

https://charts.equityclock.com/...le-mines-ltd-nyseaem-seasonal-chart

Angehängte Grafik:

agnico_prognosen.jpg (verkleinert auf 39%)

agnico_prognosen.jpg (verkleinert auf 39%)

01.03.23 09:01

#120

chivalric

charttechn. interessant

AEM ist extrem überverkauft, fundamental alles i.O., das Gap bei 54$ sollte wie ein Magnet wirken sobald die 200er bei ~48$ genommen wird. als starkes Zeichen werte ich auch, dass trotz Divi-Abschlag der Kurs gestern gestiegen ist; bin long

AEM ist extrem überverkauft, fundamental alles i.O., das Gap bei 54$ sollte wie ein Magnet wirken sobald die 200er bei ~48$ genommen wird. als starkes Zeichen werte ich auch, dass trotz Divi-Abschlag der Kurs gestern gestiegen ist; bin long

15.03.23 23:50

#121

chivalric

geknackt

die 48$ wurden heute geknackt, damit sollte es zügig bis 54$ gehen

05.04.23 13:05

#122

chivalric

passt

na das lief ja wie am Schnürchen gezogen; ideal wäre nun ein Test des gestrigen Ausbruchsbereichs bei ~52,5$. Sollte jetzt als Unterstützung dienen. Bin mit halber Position raus und Rückkauforder bei ~52,5$ ist platziert. Ggfs kaufe ich schon früher zurück, kommt drauf an wie heftig der PoG heute noch korrigiert (wenn überhaupt)

11.04.23 14:25

#124

nicco_trader

@giogen

Sieht gut aus ;-)

Vorbörslicher Handel

56,71

+0,51(+0,91%)

Vorbörslicher Handel

56,71

+0,51(+0,91%)

Angehängte Grafik:

agnico_20230411.png (verkleinert auf 40%)

agnico_20230411.png (verkleinert auf 40%)